When fuel prices are moving up and down, who is making money?

With oil markets whipping up and down—down from early October to right around Christmas, and then shooting back up since then into the first days of the new year—it begs the question: who is making money on these moves?

There are really only two parts of the petroleum sector where profitability is tied to the outright price. The first group consists of those who pull petroleum out of the ground. (And when we say petroleum, that means other products not generally considered “oil,” such as natural gas liquids, a category that includes products like propane and butane). For an exploration and production company, a price of $60/barrel (b) is better than a price of $45/b…period, end.

If you’re at the end of the equation—like if you’re a truck driver—it’s better if the price is lower. That’s pretty obvious. But at that end of the chain, there’s often a sneaking suspicion that even if the price of oil has declined, you’re not seeing all of it show up at the pump. And maybe that’s the case.

There is a long way between the commodity price of ultra low sulfur diesel (ULSD)—which trades on the CME under the symbol HO, because it used to be a heating oil contract on the New York Mercantile Exchange—and those numbers that are sitting up on a sign in front of any kind of retail outlet. More importantly, there is a long way between that CME price and the weekly Energy Information Administration/Department of Energy diesel price, which serves as the basis for the overwhelming number of fuel surcharges in the trucking sector.

There are far too many moving parts for the retail price of diesel to ever reflect in anything close to real-time the movements in the CME and the price in retail. Consider the supply chain:

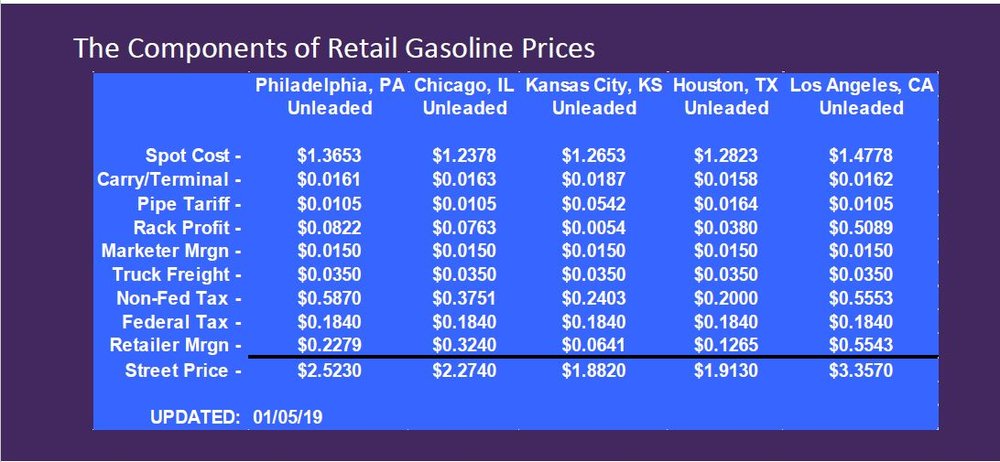

– First, we will acknowledge up front that there are more costs at each stop in the chain than the average person can begin to comprehend. What’s the cost of your workmen’s compensation insurance? What’s the rent for the service station? What are you paying truck drivers—or independent carriers known in fuel world as “jobbers”—to get the fuel from the wholesale distribution point known as the rack to the individual retail outlet? (In this article the wholesale price will be referred to as the rack price.) This chart below from EMI, a division of DTN, shows how the price of retail gasoline gets constructed. It isn’t exactly the same for diesel, but you get an idea.

– The commodity price of ULSD on the CME is for product delivered on a barge into New York harbor one month out. Here in January, February barges are getting traded. But in the spot market, which is the market reflected by price reporting agencies (PRAs) such as S&P Global Platts and Petroleum Argus, the trade might be for a barge to be delivered five days out. Under perfect market conditions, that month-out price should be higher than the spot price, because it needs to reflect the cost of storage and the time value of money. But market conditions are never perfect. The spread between the two can vary, but it tends to be just a few cents. (This writer remembers a deep freeze that struck New York years ago when barges got socked in by the ice. If you wanted a barge immediately and somebody was somehow able to deliver it, it would have cost you $1 per gallon over the commodity price. The differential generally is talked about in terms of a few cents). In recent days, PRAs are reporting that the price of U.S. Gulf Coast ULSD for delivery in the short-term has sunk well below the commodity price on the CME. It is that physical price, more than the commodity price on CME, that ultimately sets the rack price and by extension the retail price.

–How competitive is the rack fuel market in a particular region? Atlanta, right on the Colonial Pipeline that takes fuel from the Gulf Coast all the way up to the New York metropolitan area, has always been known as a cutthroat fuels market. The Rocky Mountain region, by contrast, is nowhere near as competitive and markups along the supply chain have always been known to be large. The diverging nature of competitive rack markets is why it is difficult to give an easy answer to the question of how much greater the rack price “usually” is over the CME price or the physical price assessed by the PRAs. Depending on any of those identified factors, like the competitiveness of the market, the gap between the benchmarks and the rack price can be 8-10 cents. But it might be 20-30 cents depending on the location.

—But even if the CME or the PRA price plummets, what’s to stop the seller of diesel or any other fuel at the rack from simply keeping the price higher? The answer is competition. It can’t happen because a seller trying to cling to that higher price is competing with sales of diesel or gasoline that are getting done on a price tied to a PRA price. If you’re a buyer at the rack, you can buy at a company’s rack price or you can buy on a formula tied to the PRA price.

For example, in the Atlanta market, a sale of gasoline might be made on some sort of formula tied to the posted price of Shell in Atlanta, or it might be tied to a price based on the S&P Global Platts or Petroleum Argus spot market price, plus a premium. If Shell holds that rack price high in the face of the declining commodity and spot price, its fuel could be uncompetitive in literally a day’s time because the PRA price will move down to reflect the actual market. The reality is the speed of the market requires that companies adjust their rack prices one or two times per day to stay competitive. It’s reasonable to assume that the rack price will move in close to a lockstep fashion with broader commodity and spot market moves. It shows the ULSD rack price reacting quickly to the market increase in ULSD on CME after December 24, but also shows it reacting just as quickly to the downside as the market headed toward its recent Christmas Eve low.

—After that, it gets tricky. Oil companies do not generally own the retail stations that bear their name. They are owned by individual companies—or sometimes individual human beings—who have chosen to “brand” their outlet with a name like Exxon. They are required to buy all their fuel from the Exxon rack distribution network, another reason why the rack prices charged by the oil companies need to stay competitive. If they don’t, their branded operators are going to be at a competitive disadvantage to other stations, they won’t be happy, and they will be more likely to sign up with another company when the branded contractual relationship comes to an end. (The alternative to being branded is to be unbranded, a situation in which the station can buy fuel from whatever supplier it wants. Ironically, some of the biggest retailing brand names out there—think Wawa or Casey’s—are actually unbranded because they are not directly tied to a specific fuel supplier).

One thing the branded station owners aren’t required to do is set a price dictated by the fuel supplier. If they get too out of line they might get an unpleasant telephone call from their branded supplier, but otherwise, they’re on their own. So the question then posed by truck drivers might be whether those retail prices are staying in line with movements in the commodity and spot markets.

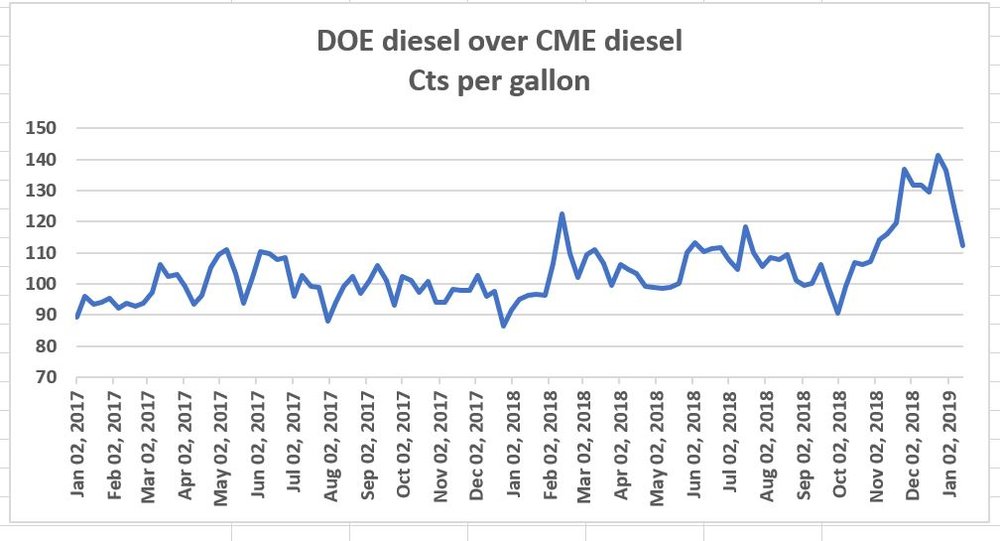

Consider this next graph of the last two years. It shows the spread between the weekly DOE diesel price that is the basis for many fuel surcharges against the price of ULSD as traded on the CME. The higher the point on the graph, the more out of whack with the trend in commodity prices the DOE number is to the upside. (And if it’s out of whack, don’t blame the DOE; it just does a survey).

What you can see from this is that the gap between the DOE diesel price and the CME ULSD price has tended to run in a fairly wide but mostly consistent range of 90 cents to $1.05/gallon. It held there for most of 2017. Given the thousands of retail outlets out there, each with their own competitive situation on highways and major intersections, a range of 15 cents/g as a consistent parameter doesn’t seem too volatile.

But look at the past few weeks. From November 12 through Christmas Eve, the CME ULSD price plummeted almost 50 cents/gallon. But the DOE retail diesel price dropped just 23.3 cents, as retail prices never move that fast in reaction to such enormous spot and wholesale changes. The result was that the DOE price released Christmas Eve was about $1.40 more than the CME ULSD price for that day, far above the norms. But in just two weeks, that $1.40 spread became $1.23 as retail prices continued to sink in typical delayed reaction. That spike has started to move back toward a rough norm as CME ULSD prices have staged a remarkable comeback following the December 24 low. The DOE retail price has not reacted yet; its latest issuance, on January 14, continued a downward trend.

—The charge levied against station owners is that they’re not quick enough to reduce their prices in a falling market, as if the average person knows the complicated cost structure of the diesel supply chain and how fast prices should come down. And yes, the owners of those stations are not going to want to be too quick to reduce their prices. What business is? But based on the fact that since December 24 spot and wholesale prices both rose significantly while retail prices—according to the DOE—fell through at least the first days of January could be interpreted that this time around, retailers were too slow to raise their prices.

—One thing you can take out of the equation is the idea that a retail station in a rising market is selling gasoline it purchased a week (or more) earlier at a price well above what it paid. The gap between deliveries of fuel into truck stops and retail outlets gets measured in hours or at most a day or two if they’re small. Nobody’s selling stuff they got a few weeks ago because like any business, a retail fuels outlet doesn’t want to bear the cost of keeping inventory, so they’ll be happy to take it as they need it, and not too much more. They don’t have “stuff” from a few weeks ago.

—So if the retail outlets weren’t generally able to be winners selling diesel they had lying around for weeks, who were the winners in the recent price movements, with retail prices slow to match the commodity markets? Nobody, unless you declare as a winner any consumer that purchased fuel at the retail level at a number significantly less than where a general “norm” might dictate.

A professional trader can take advantage of small opportunities in liquid markets where an arbitrage opens up, like on the CME or in active derivatives markets tied to physical prices. To take advantage of an arbitrage in spreads on the wholesale and retail supply chain is far more difficult. That’s one of the reasons why so much pricing to sell fuel for trucking gets done on some sort of automatic pilot. It could mean a contractual agreement for a fleet to buy diesel at a particular truckstop chain at the DOE price plus—or even minus—a differential, or maybe it buys diesel on a formula tied to the rack price or a PRA number. It’s the smaller fleets or the independent owner-operators who don’t get the advantage of that most of the time. They buy at the price that’s sitting out in front of the station, which had a lot of steps to be taken before getting to that final number.